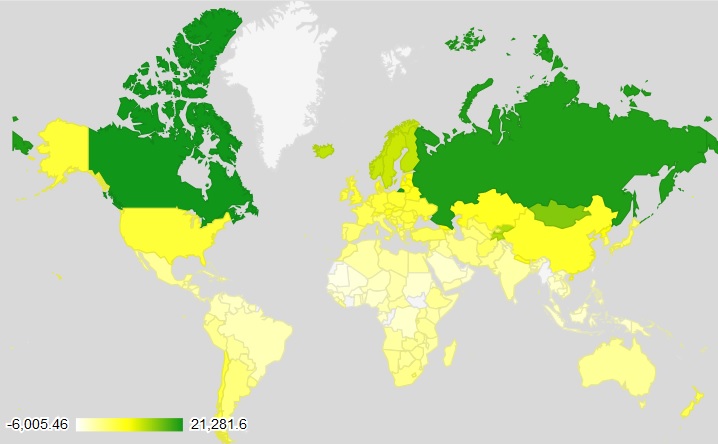

Graph 1: Overall climate change winners

The implementation of climate stability accounts for the most challenging contemporary global governance predicament that seems to pit world countries but also today’s generation against future world inhabitants. In a trade-off of economic growth versus sustainability, a broad-based international coalition could establish climate stability. As a novel angle towards climate justice, the attention to global warming gains and losses being distributed unequally around the globe (Puaschunder, 2017) allows to propose to search for a well-balanced climate mitigation and adaptation public policy mix guided by micro- and macroeconomic analysis results.

The ‘Climate in the 21st Century‘ endeavor therefore offers a new way of funding climate change mitigation and adaptation policies but also the transition to renewable energy through broad-based climate stability bonds-and-taxation mix that also involve future generations (World Bank, 2015).

Having shed light on the gains of a warming earth demands for the redistribution of climate change benefits to those areas of the world that will be losing from a warming earth. In the implementation, a climate change bonds but also taxation strategies are recommended. Having found that there are gains from a warming earth demands to transfer benefits into areas of the world that will be primarily losing from climate change. In order to avoid governmental expenditure on climate change hindering economic growth (Barro, 1990); the climate transfers should be enacted through bonds and taxes.

First Jeffrey Sachs (2014) proposed an intergenerational burden sharing idea by presenting a 3-model climate change burden sharing through fiscal policy with bond issuing in order to reflect the implementation regarding contemporary finance and growth models with respect for maximizing utility of the model. In an overlapping-generations type model, research should elucidate climate change abatement and mitigation policies to lead to a fairer solution across generations. The current generation mitigates climate change and provides infrastructure against climate risk financed through climate bonds to be paid by future generations. Since for future generations the currently created externalities from economic activities – the effects of C02 emissions – are removed, this entails that the current generations remain financially as well off as without mitigation while improving environmental well-being of future generations. As Sachs (2014) shows, this intergenerational tax-and-transfer policy turns climate change mitigation and adaptation policy into a Pareto improving strategy. Shifting the costs for climate abatement to the recipients of the benefits of climate stability appears as novel, feasible and easily-implementable solution to nudge many overlapping generations towards future-oriented loss aversion in the sustainability domain (Puaschunder, 2016a).

One of the most prominent forms to create revenues for public long-term investment causes are taxes. Taxation is codified in all major societies and a hallmark of democracy. Aimed at redistributing assets to provide public goods and ensure societal harmony, taxation improves societal welfare and fairness notions within society. Tax compliance is a universal phenomenon based on cooperation in the wish for improving the social compound. Taxpayers voluntarily decide to what extent to pay or avoid tax that limit the personal freedom. In a social dilemma, individual interests are in conflict with collective goals. From a myopic economic perspective, the optimal strategy of rational individuals would be to not cooperate and thus evade tax. Short-term the single civilian tax contribution does not make a significant difference in the overall maintenance of public goods – if only a few taxpayers evade taxes, public goods will not disappear or be reduced. But if a considerable number of taxpayers do not contribute to tax over time, common goods are not guaranteed and ultimately everyone will suffer from suboptimal societal conditions (Dawes, 1980; Stroebe & Frey, 1982; Puaschunder, 2015a). Contemporary economic research has focused on costs and risks of tax evasion (Tyler & De Cremer, 2006). Coercive means – such as audits and fines – were found to crowd out tax morale and ultimately result in greater non-compliance as people feel controlled and not being trusted (Cialdini, 1996; Feld & Frey, 2002; Frey, 1992; Hasseldine, 1998). In the last decade, researchers have started to recognize the importance of incorporating morals and social dynamics in economic theory on tax behavior (Andreoni, Erard & Feinstein, 1998). When analyzing tax behavior, recently behavioral economics insights have drawn attention to social influences (Puaschunder, 2015a).

Behavioral economists widen the lens of incorporating sociological and socio-psychological notions of fairness stemming from social comparisons regarding tax burdens could be positive drivers of tax compliance to overcome the ‘burden of taxes’ and associations of losses. The cases of voluntary, self-chosen tax ethics and situational influences on social tax compliance norms have just recently been covered by behavioral approaches towards public administration. In general, social comparisons determine social norms that define internalized standards how to behave. Yet internalized social norms are based on comparisons with others that may determine tax morale (Frey, 1997; Mumford, 2001; Schmölders, 1960). Social norms elicit concurring behavior when taxpayers identify with the goals of a group but also if they feel being treated in a fair manner by that group. Social fairness considerations in a tax reference group may further taxpayer compliance. Fairness is believed to decrease egoistic utility maximization leveraging trust and reciprocity as interesting social norms building factors (Kirchler, 2007). Social perceptions of fairness as underlying social norms are therefore potential tax ethics nudges. But psychological facets of fairness for the formation of social norms have been left out. If taxpayers believe that non-compliance is a widespread and socially-accepted, then it is more likely that they will not comply as well. Non-compliance may stem from the notion of unfairness in how the tax burden is weighted heavier on some parts of society.

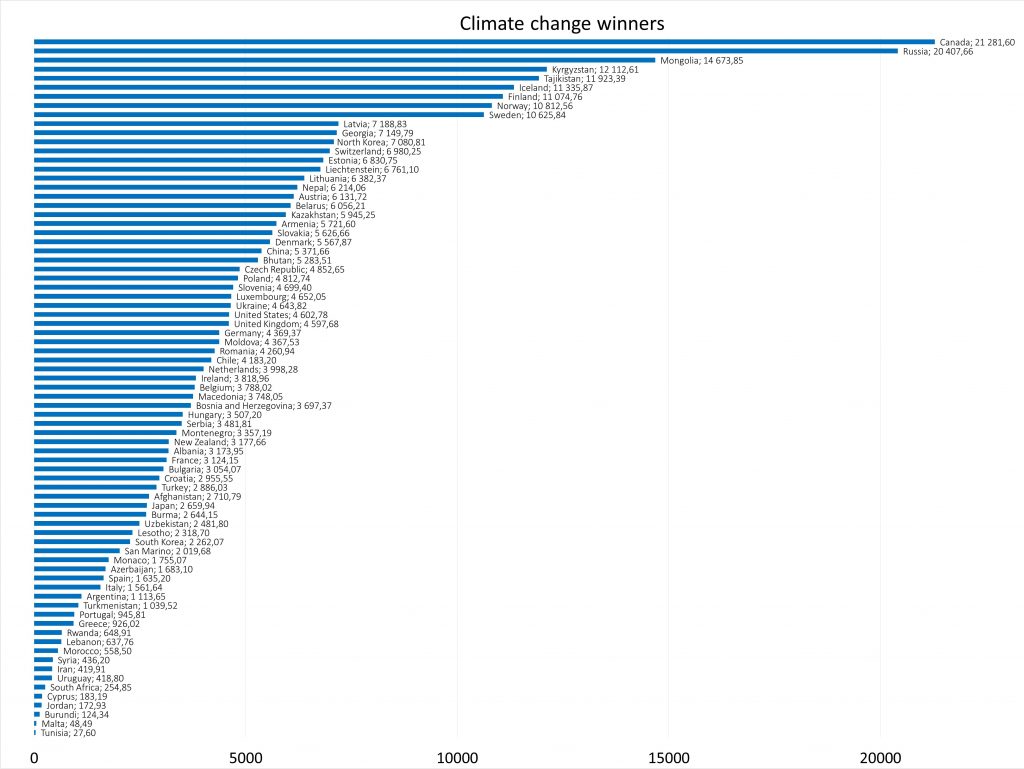

The respective bonds-and-tax climate stability financing strategy therefore proposes to bear the burden of climate in a right, just and fair way around the globe. In the climate change winner countries, taxation should become the main driver over financing climate stability strategies. Foremost, the industries winning from a warming climate should be taxed. The Winner-Loser-index is based on the cardinal temperatures for all GDP contributing sectors. Based on the cardinal temperatures for the three GDP components agriculture, industry and service, the taxation should be enacted for those sectors having most time ahead. The rational is that these sectors will be gaining the most from a warming earth and will therefore be flourishing.

The taxation models should aid to share the burden of climate change within society in a fair way. Regarding concrete climate taxation strategies, a carbon tax on top of the existing tax system should be used to reduce the burden of climate change and encourage economic growth through subsidies (Chancel & Piketty, 2015). Within a country, high and low income households should face the same burden of climate stabilization adjusted for their disposable income. First, climate justice within a country should pay tribute to the fact that low- and high income households share the same burden proportional to their dispensable income, for instance enabled through a progressive carbon taxation. Those who caused climate change could be regulated to bear a higher cost through carbon tax in combination with retroactive billing through inheritance tax. But also developed and underdeveloped countries as well as various overlapping generations are affected differently. Besides progressive taxation schemes to imbue a sense of fairness in climate change burden sharing, inheritance taxation is also a flexible means to reap past wealth accumulation, which potentially caused environmental damage. The burden of climate change mitigation and adaptation could also be allocated in a fair way within society through contemporary inheritance tax in order to reap benefits of past wealth accumulation.

In addition, finding the optimum balance between consumption tax adjusted for disposable income through a progressive tax scheme will aid to unravel drivers of tax compliance in the sustainability domain. If climate taxation is perceived as fair and just allocation of the climate burden, this could convince tax payers to pay one’s share. A novel ‘service-and-client’ atmosphere could promote taxpayers as cooperative citizens who are willing to comply if they feel their share as fair contribution to the environment. Taxpayers as cooperative citizens would then be willing to comply voluntarily following the greater goal to promote taxpayer collaboration and enhance tax morale in the environmental domain. International comparisons of tax behavior also reveal tax norms being related to different stages of institutional development of the government, which is an essential consideration in sharing the climate change burden in a fair manner between countries. A completely novel approach is to shed light on the benefits of a warming earth in order to derive fair climate gains distribution strategies around the world (Puaschunder, 2017).

Graph 2: Climate Change Winners weighted by GDP/capita